Australian property markets are entering a period defined by a tension between strong underlying demand and constrained near-term delivery. Across office, industrial, retail, and residential sectors, occupier and buyer demand remains robust creating substantial pent-up demand for existing stock. Yet the pipeline of new supply to meet this demand has thinned materially across all sectors, challenging the feasibility of new developments. This tension of strengthening demand against a thinning pipeline is establishing a foundation for a sustained period of rent growth across most sectors over the medium term.

A Subdued Development Pipeline Across All Sectors

The reduction in new supply is a cross-sector phenomenon. For office and industrial, it follows a period of elevated completions as projects committed during years of strong rent growth and favourable capital market conditions continue to work their way through the pipeline. That pipeline is now largely exhausted, and the rising cost environment has deterred the new commitments needed to sustain supply levels.

National office completions are expected to average approximately 160,000 sqm per year between 2026 and 2030 which is 64% below the 10-year historical average. Meanwhile, eastern seaboard industrial completions in 2026–27 are averaging 1.7 million sqm which is more than 10% below the 10-year average. As a result, the coming years will mark a meaningful step-down in delivery across both sectors, even as underlying demand continues to build.

Residential development faces analogous pressures. Despite targeted government intervention to accelerate housing supply, feasibility barriers have kept construction activity well below what population growth demands. Development is largely concentrated in select submarkets — Sydney’s inner north and east being a prime example — where prices are high enough to cover elevated construction costs. Elsewhere, it is much more difficult to make the feasibility equation stack up.

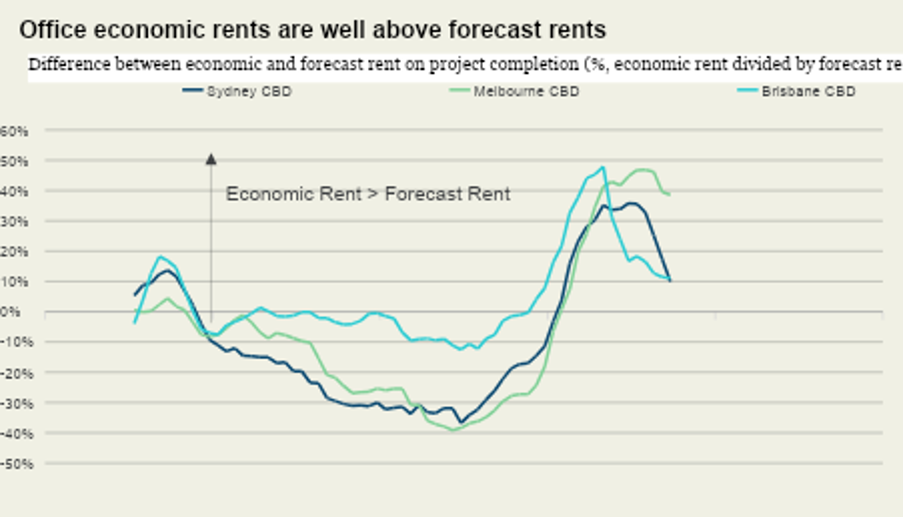

The Feasibility Gap: Where Economic Rents Meet Reality

Central to understanding this supply slowdown is the concept of the economic rent — the minimum rent required to justify new development after accounting for construction, land, financing, and return requirements. Across office and industrial markets in every major Australian capital city, economic rents currently sit above where rents are forecast to be at the time of a new building’s practical completion. In practical terms, a developer who commits to a project today faces a meaningful probability of not achieving the rent needed to make the numbers work.

The gap between economic and achievable rents has widened as construction costs have risen sharply since 2021, driven initially by global supply chain disruptions and subsequently by sustained domestic cost pressures. Some material prices have increased by more than 70% since early 2021, while construction labour wages have risen approximately 19% over the same period. Given that construction costs are typically largest variable input in development feasibility, these increases have had an outsized effect on the economics of new supply.

Geopolitical Risk as a New Source of Cost Escalation

Construction cost growth, having already reached elevated levels, is showing signs of renewed acceleration. According to Rawlinsons, costs rose 4.7% over the year to Q4 2025 which is a concerning reacceleration after a period of moderation. Against this backdrop, the escalation of conflict in the Middle East introduces an upside risk through its impact on global oil prices.

Oil is a pervasive input across the construction supply chain. Higher prices are already flowing through to a broad range of building materials, including PVC piping, concrete, and glass which are all embedded throughout commercial and residential structures. The transmission mechanism is direct and further complicates the feasibility equation for developers.

Knight Frank’s modelling quantifies this exposure. A 10% increase in total construction costs for a new premium office tower raises the required economic rent by approximately 5%. For a prime industrial development, the same cost shock translates to a 4% increase in economic rents. At a time when the feasibility gap is already meaningful, further cost inflation narrows the window for viable new development further still.

Rent Growth: The Realistic Path to Feasibility

The path back to a functioning development pipeline runs primarily through rent growth, rather than cost reduction or yield compression. Interest rates have risen and are currently expected to fall in late-2027 or in 2028, limiting the kind of yield compression that would materially improve capital values and development returns. Construction costs, meanwhile, are historically resistant to outright decline — they are sticky on the way down in a way they are not on the way up. The more plausible near-term scenario is one of cost growth moderating to below-inflation levels, which would deliver a gradual improvement in real feasibility over time.

Rent growth is therefore the expected to be the required lever. With limited new stock entering markets across most sectors, vacancy rates are declining and occupier competition for quality space is intensifying. This is most visible in the prime office segment, where annual net effective rental growth in the best-located areas of Sydney and Melbourne CBD is running at 14% and 16%, respectively.

For residential developers, the same logic applies. Tight rental market conditions and strong underlying demand in major cities provide the economic rationale for feasibility to improve, even if the path requires patience. Government efforts to ease planning constraints and reduce holding costs remain important enablers, but cannot substitute for the market fundamentals that ultimately determine whether a project proceeds.

Outlook

The Australian property development sector is in the early stages of a period of constrained supply, elevated feasibility thresholds, and a geopolitical environment that adds tail risk to an already-high construction cost base. For commercial and residential developers alike, the near-term outlook is one of selective opportunity rather than broad activity. Developers should focus on markets and asset classes where outlook for rental growth is strongest and the gap between economic and achievable rents is narrowing fastest. Beyond the near term, the growing supply shortfall is laying the foundation for stronger rent performance and improved market conditions over the medium-term.

{kind=link}